Why residential mortgage lenders should look more at energy labels

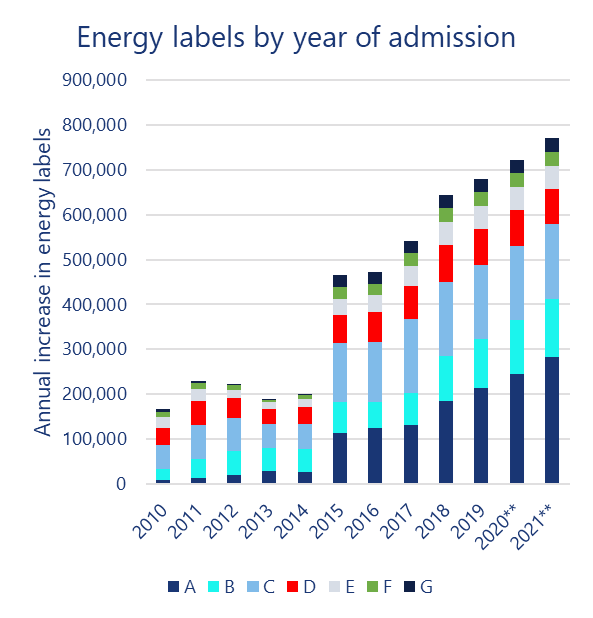

In a world where green investing is booming business, the Dutch housing market is embracing energy labels. Within five years, we saw a 43% increase in energy labelled homes. Energy labels have both green and financial significance. Houses are labelled “A” to “G“ with “A“ being the most energy efficient.

Roodhals Capital investigated the financial aspects of applying such a label to your house. Having your house labelled “A” instead of “G” can increase the market value by almost 14%, which partially explains the 10-year trend of decreasing Loan-to-Values. Today, virtually all newly constructed houses are “A” labelled. Consequently, a correlation ensues between the rise in use of energy labels, increasing house prices and mortgage volumes. This relationship became significant in 2016 and seems to be strengthening. Variables such as interest rates and structural home shortages also influence house prices, causing us to remain careful to reach bold conclusions. Nonetheless, we ask ourselves if mortgage lenders are doing enough to apply the improved use of energy labels to their mortgage offering?

>

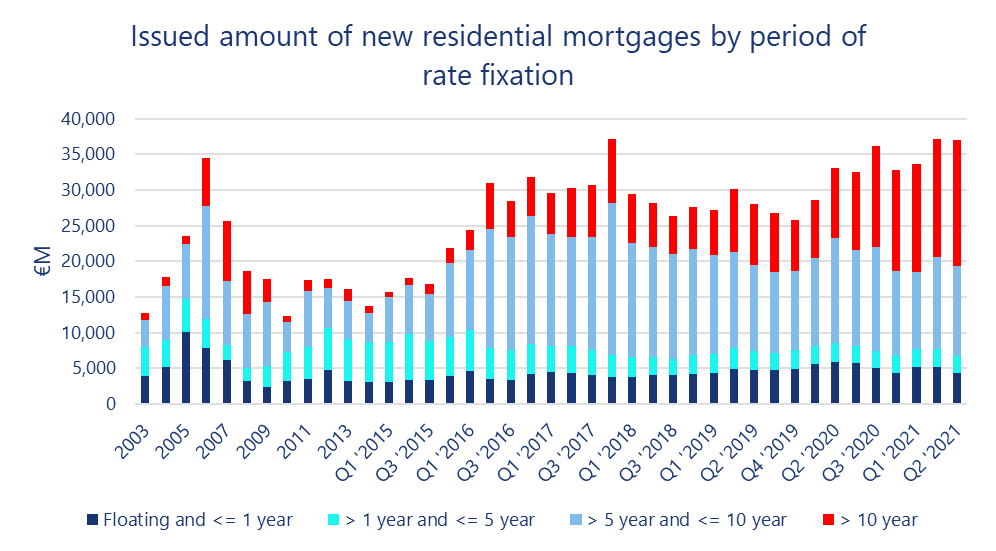

In spite of rising house prices, mortgage lending remains robust. In fact, we saw over a tenfold increase of mortgages with a rate fixation of 10 years or more between 2011 to 2021. Mortgages, and especially those with a longer rate fixation, seem to be popular due to persistently low interest rates. Or is there more to it?

We believe two other aspects play a role here. One is the emergence of non-bank lenders, such as pension funds and insurance companies, who favour longer dated mortgage loans. The other, we argue, is the energy label. The correlation between the rapid growth of labelled houses and longer tenor mortgages is no coincidence. Homes with a label between “A” and “C” will and should be more affordable and pose less risk to the lender (assuming comparable LTV’s). Moreover, the rapid growth in residences labelled “A” to “C” is not only explained by new construction. Homeowners also invest in home improvement.

We see a variety of mortgage products that offer a reward for a high energy label, particularly the “A” category. But relatively few offerings that reward owners or buyers of unlabelled or lowly labelled dwellings to make improvements that de-risk the lender. Even while the trend supports it and while that is a substantial share of market. At Roodhals we believe that having a mortgage offering that caters to improving energy labels adds value in a competitive market.

Want to know more? Contact us via the website.

**Roodhals forecast

Sources: Roodhals Capital; Rijksdienst Voor Ondernemend Nederland (2021); DNB (2021); Brounen, D., & Kok, N. (2011), het energielabel op de koopwoningmarkt

We thank Rebecca Baijer for her contribution to this article