SME finance at a crossroads

While it seems as though the major banks in the Netherlands continue to bid farewell to their SME customers year in, year out, non-bank SME financing is steadily growing. Although the market share is not as convincing as in the residential mortgage sector, according to the SME Financing Foundation (SMF), the market share in 2022 rose to about 11% of all SME financing. Non-bank financing grew by 21% last year to a total of €3.9 billion.

These figures are not solely due to retreating commercial banks. In our view, it is primarily technological developments that are opening new financing channels for Dutch entrepreneurs. Consider FinTech solutions in the field of payment transactions, real estate financing, online banking and financing, and transaction or capital markets services. For more information, we refer you to our FinTech monitor. You can find and subscribe to this quarterly report here.

With SME financing, credit analysis is also changing. Digital lending platforms are leading in the use of PSD2, AI and data-driven credit analysis. Some challenger banks such as Bunq have had to enforce their use of data-driven analyses through the courts after the DNB tried to stop this development. Of course, these models will only become stronger over time as more cyclical data becomes available.

Nevertheless, the phenomenon of retreating banks remains striking. FD measures that the three major banks have seen their exposure to SMEs decrease by 16% over the last 10 years. For small businesses, this was even -39%. The costs of compliance are often mentioned. But in fact, the business model is broken because risk-based pricing for SMEs has failed. If all costs, including provisions and write-offs for defaults and compliance, are included in the price, could the tide then be turned? FD quotes Professor Lex van Teeffelen as saying that a lack of competition is at the root of this. Be that as it may, we note a lack of motivation among the major banks to further develop the business case for SME financing.

Are we really going to establish a state bank for SMEs in this era of FinTech?

With some disbelief, we look at the political repair job that is now culminating in the desire to simply establish a new SME state bank. Or that De Volksbank would like to take up this baton. The cause is more likely to be excessive regulation in the financial sector. Rather stimulate new FinTech initiatives by helping them grow with the right regulation and funding. Perhaps Invest-NL can play a role in this.

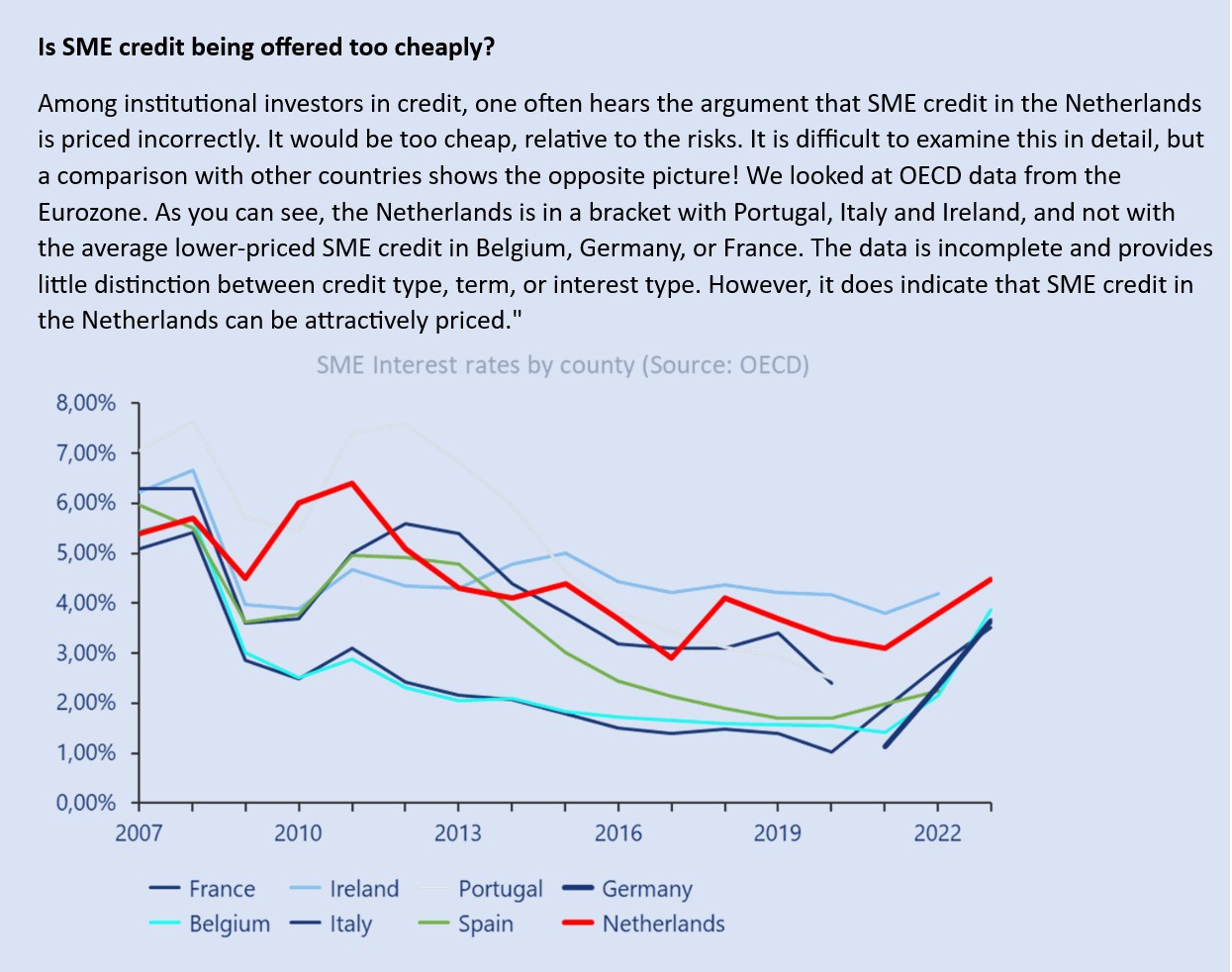

Risk-based pricing

Still, a quick return to risk models. Particularly important for SME financing is a good stratification of SMEs into risk classes. The aim is to implement a sustainable interest policy. FinTech can be of great help in this. The number of data points that can be continuously monitored by small lenders is the backbone of the disruption being proclaimed.

However, the development of SME financing is progressing slower than expected. Why is that? That's not a simple question. The main reason we see is that SMEs need financial services. The big banks were quite good at this. Relationship banking, with payment transactions, payroll accounts, working capital financing, guarantees, loans and advice, was a one-stop financial solution that was also reasonably cheap.

FinTech and non-bank financiers usually have a much narrower range of services. One handles payment transactions, others finance real estate, and for debtor financing, the entrepreneur must turn to a third party.

In our view, we are on the eve of a revolution in SME financing. We are mainly referring to the emergence of non-bank SME financiers offering a broad range of services. This opens up a much larger share of the SME market. The challenge lies mainly in the funding model that matches this, and less in the technical possibilities.

The funding model for many non-bank financiers is based on mono-line products structured for specific groups of investors, such as pension funds, insurers, wealthy individuals, etc. To set up a broad financial service package for SMEs, we expect that the balance sheet of the FinTech platform itself will play a much more important role. Look at it this way: if investor 1 finances SME A's property and investor 2 finances her debtors, a "relationship" between these creditors arises that the platform must manage. This is very common for banks. For non-banks, this is now a hurdle that will undoubtedly be overcome.

Credit Buffs

In all this big data and AI activity, we specifically call for attention to the human dimension. In jargon: the duty of care. Not everything can be read from numbers. The traditional skill of assessing a business and its people remains important. It's a mix of quantitative and qualitative factors, measurable and non-measurable variables, and experience. SMEs are characterized by diversity, even more than individuals. There are so many company-specific or sector-specific factors that a data-driven model will only be effective for a sub-area.

Without human insight into credit assessment, it is still difficult to accurately assess all conditions for an SME loan. Much of the monitoring is increasingly automated, but intervention in (possible) defects is still human work. The same applies to SME lenders as it does to consumer credit: engage in dialogue with your customer in a timely manner.

“Computer says no”

Finally, the question of whether generative AI engines can take over credit work? The fact is that AI is making an entrance into credit assessment. You already see investment managers actively experimenting with generative AI in compiling equity portfolios and assessing spreads on everything from interest, commodities or horse races, to name a few. As we also see in algorithmic trading, arbitrage profits from generative AI will gradually disappear.

Here too, we expect the law of arbitrage opportunities to apply. We do not belong to the advisors who say that it won't be that bad. However, we will sharply assess whether the engines lead to excesses or the demise of the human dimension.

How can we help you?

Roodhals helps (non-) banking institutionswith funding and advises on strategy for funding and growth.

If your company faces financing issues or you are seeking capital to implement your plans, please do not hesitate to contact us.

You can contact us here.